Broadband Breakfast reported on June 2, 2026 that BEAD winners are expected to put up nearly $11.4 billion of their own capital, covering more than 37% of project costs against a 25% floor. That shifts BEAD procurement math in a very practical way. Once an operator is writing a much larger check, the cheapest compliant vendor stops looking clever and starts looking dangerous.

Higher BEAD Match Rewrites Procurement Math

The grant-era story was eligibility. The live deployment story is capital efficiency. NTIA’s post-2025 Benefit of the Bargain structure pushes states toward minimal BEAD outlay, so applicants now win by asking for less federal money without handing themselves a construction mess a few months later.

That changes vendor selection. Buyers are no longer comparing BOMs on unit price alone. They are comparing schedule risk, domestic-compliance paperwork, labor availability, and how much rework a partner is likely to create after award.

Cheap Vendors Now Look Expensive

When more operator cash sits in the stack, procurement teams start pricing failure properly. A late fiber shipment, weak BABA documentation, or a contractor that misses make-ready assumptions can burn more value than a slightly higher bid from a supplier that can actually deliver. That is why BEAD is starting to look less like a subsidy race and more like disciplined network connectivity procurement.

The real screen is whether a vendor helps reduce grant ask per passing without raising execution risk. That sounds obvious, which is probably why so many organizations ignore it until the spreadsheet meets the field.

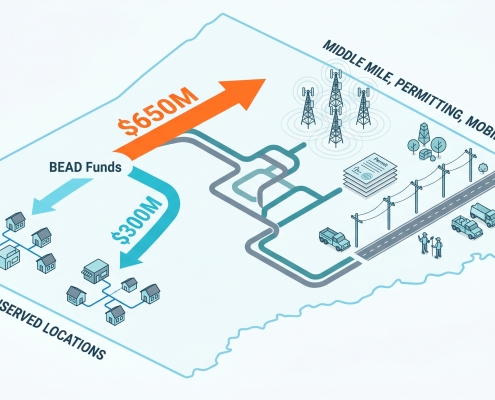

Address Planning Hits the Critical Path

There is also a quieter infrastructure consequence. Operators funding more of the build have less tolerance for turn-up delays caused by weak address planning, messy inventory, or routing cleanup that should have been handled during design. Clean IPAM moves upstream fast when every avoidable truck roll comes out of your own capex.

The same goes for service-edge policy. A bad address plan, sloppy route objects, or weak BGP security can turn a funded build into an activation delay. That does not make BEAD an IPv4 story, but it absolutely makes IPv4, routing, and provisioning part of the procurement discipline.

Scale Gives Large Operators a Bid Edge

ACLP’s analysis, as cited by Broadband Breakfast, said a dozen national ISPs with footprints above 2 million locations are expected to contribute about $6.1 billion, more than roughly 400 other BEAD participants combined. That is procurement leverage in plain English. Bigger operators can spread engineering, finance, and supplier negotiations across a wider footprint, which lets them bid harder without pretending risk has disappeared.

Smaller providers can still win, but the bar is clearer now. They need tighter designs, cleaner supplier stacks, and financing that survives reopened rounds where states must evaluate bids within 15% of the lowest BEAD outlay before secondary criteria matter. In a $42.45 billion program, that is enough to turn procurement discipline into market share.

FAQ

What do higher BEAD matching funds change for operators?

They force operators to treat procurement as capital protection, not just grant compliance, with more scrutiny on vendor reliability, schedule control, and downstream operating cost.

Why does BEAD procurement math favor larger providers?

Larger providers usually have lower capital costs and more purchasing leverage, which helps them self-fund more of the project while keeping bids competitive.

How does IPv4 planning relate to BEAD-funded builds?

New service areas still need clean addressing, inventory control, and realistic route policy, and those issues get expensive fast if they are postponed until activation.

What should smaller BEAD applicants focus on now?

They need tighter cost models, suppliers that can prove compliance and delivery, and network designs that avoid rework after award.